International Standards on Auditing: ISA200 - Overall Objectives of the Independent Auditor

What is the meaning of Financial statements?

Financial Statements is “a structured representation of historical financial information, including related notes, intended to communicate an entity’s economic resources or obligations at a point in time or the changes therein for a period of time in accordance with a financial reporting framework”.

What is Audit Risk?

“The risk that the auditor expresses an inappropriate audit opinion when the financial statements are materially misstated”

What is Detection risk in an audit of financial statements?

Detection risk is “the risk that the procedures performed by the auditor to reduce audit risk to an acceptably low level will not detect a misstatement that exists and that could be material, either individually or when aggregated with other misstatements”

What is Professional skepticism?

“An attitude that includes a questioning mind, being alert to conditions which may indicate possible misstatement due to error or fraud, and a critical assessment of audit evidence”

What is the purpose of conducting an Audit in Accordance with ISAs?

“The ISAs provide the standards for the auditor’s work in fulfilling the overall objectives of the auditor”

What should the auditor do if an objective in a relevant ISA cannot be achieved in an audit of financial statements?

If an objective in an ISA relevant to the audit cannot be achieved the auditor shall evaluate whether it prevents the auditor from achieving the overall objectives of the auditor and thereby requirements of other ISAs. The auditor has to see whether it requires the auditor to modify the auditor’s opinion or withdraw from the engagement. Failure to achieve an objective is a significant matter requiring documentation in accordance with ISA 230.

(Note: The author is the partner of AK & Partners Auditors and Chartered Accountants, one of the leading auditing firms in qatar. Contact: 33106154)

recent posts

-

Qatar Income Tax: Obligation to Prepare and Preserve Books of Accounts

Accounting helps to ascertain the profits of the business. Whether small or large, every b

-

Withholding Tax and Filing Requirements in Qatar

Withholding tax is the tax on income earned by a person who is not a resident of the State

-

How to Achieve the most ambitious goals

Every person has goals to achieve sometimes we succeed in achieving them sometimes not and

-

Turning Challenges into Opportunity; How STARBUCKS Survived the Economic Recession of 2008

Rumors are spreading everywhere about economic recessions and their impact. When we think

-

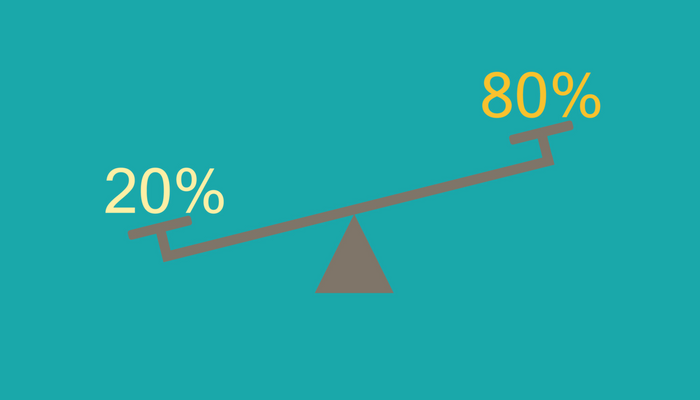

Seven Key Areas in Your Business where You Can Apply the 80 - 20 Rule

The 80-20 rule, also known as the Pareto Principle, says that 80% of outputs result from 2

-

5 Factors which shows how ‘Teamwork’ leads to Business Success.

The ancient Pyramid of Giza is said to be one of the seven official wonders of the